> For the complete documentation index, see [llms.txt](https://hapi-one.gitbook.io/hapi-protocol/llms.txt). Markdown versions of documentation pages are available by appending `.md` to page URLs; this page is available as [Markdown](https://hapi-one.gitbook.io/hapi-protocol/overview/aml.md).

# AML and Cryptocurrency

The imperative and crucial notion of cybersecurity hinges on compliance-ready solutions. CEX incorporates a slew of preventative measures in hope of keeping exchange regulations compliant. One of the most common approaches towards eliminating any underhanded schemes is KYC. KYC creates an impediment for money launderers by instituting an identity disclosure that allows for easily traceable detection of potentially fraudulent activity. This however can be considered a "passively" constructed attempt at preserving compliance rather than proactively contending with the problem itself. It can be reasoned from the fact that AMLD5 (Anti Money Laundering Directive 5) is inundated with a plethora of blind spots that can quite handily be exploited either by the design of its inherently flawed structure or insufficient collaborative endeavors from the local and international regulatory bodies.

The vastness of the issue exacerbates further if we are to consider that the backbone of the KYC is private data aggregation that impedes the decentralized undertone of the cryptocurrency market. This coupled with mediocre security and constant leakage of private data is the scourge of the privacy conformant and conscious individuals. The conclusion made by Houben and Snyer: “\[...] this approach is not very convincing if the legislator is truly serious about unveiling the anonymity of cryptocurrency users to make the combat against money laundering, terrorist financing and tax evasion more effective”. In order to preserve the solidity of the non-custodial nature of the digital currency market, there is an increasingly salient demand for, if not total substitution of the currently imposed and nascent suggested measures but at the very least a supplementary decentralized tool that would aid in promoting fair and compliant environment. With the emergence of the new type of financial instruments and subsequent adoption of these instruments by a wider cohort of people, there is a patent need for revisitation and reassessment of the customarily enacted compliance mechanisms and their applicability to the new paradigm of financing and investing. This is in part what Edward Kane means by referring to regulatory dialectics.

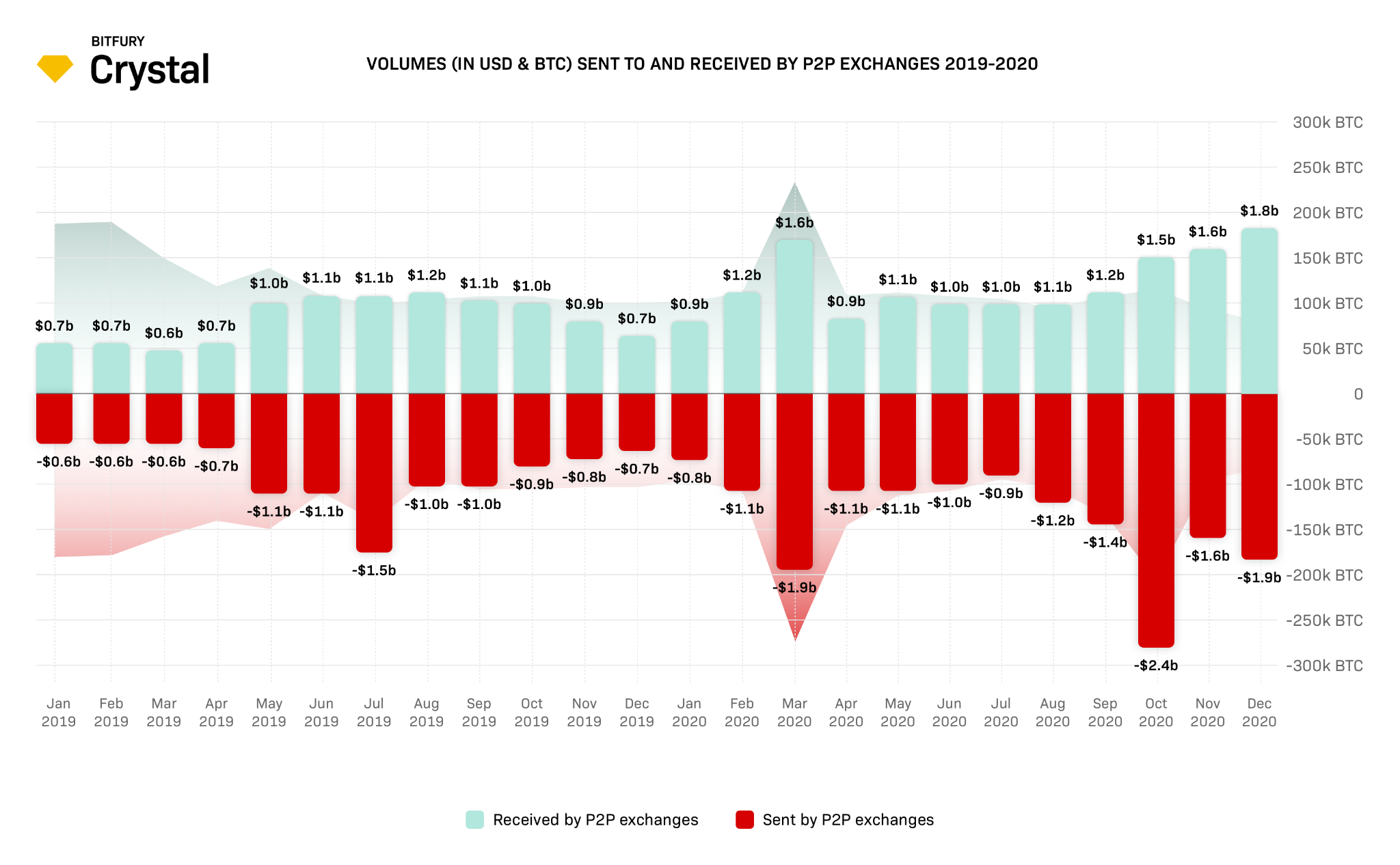

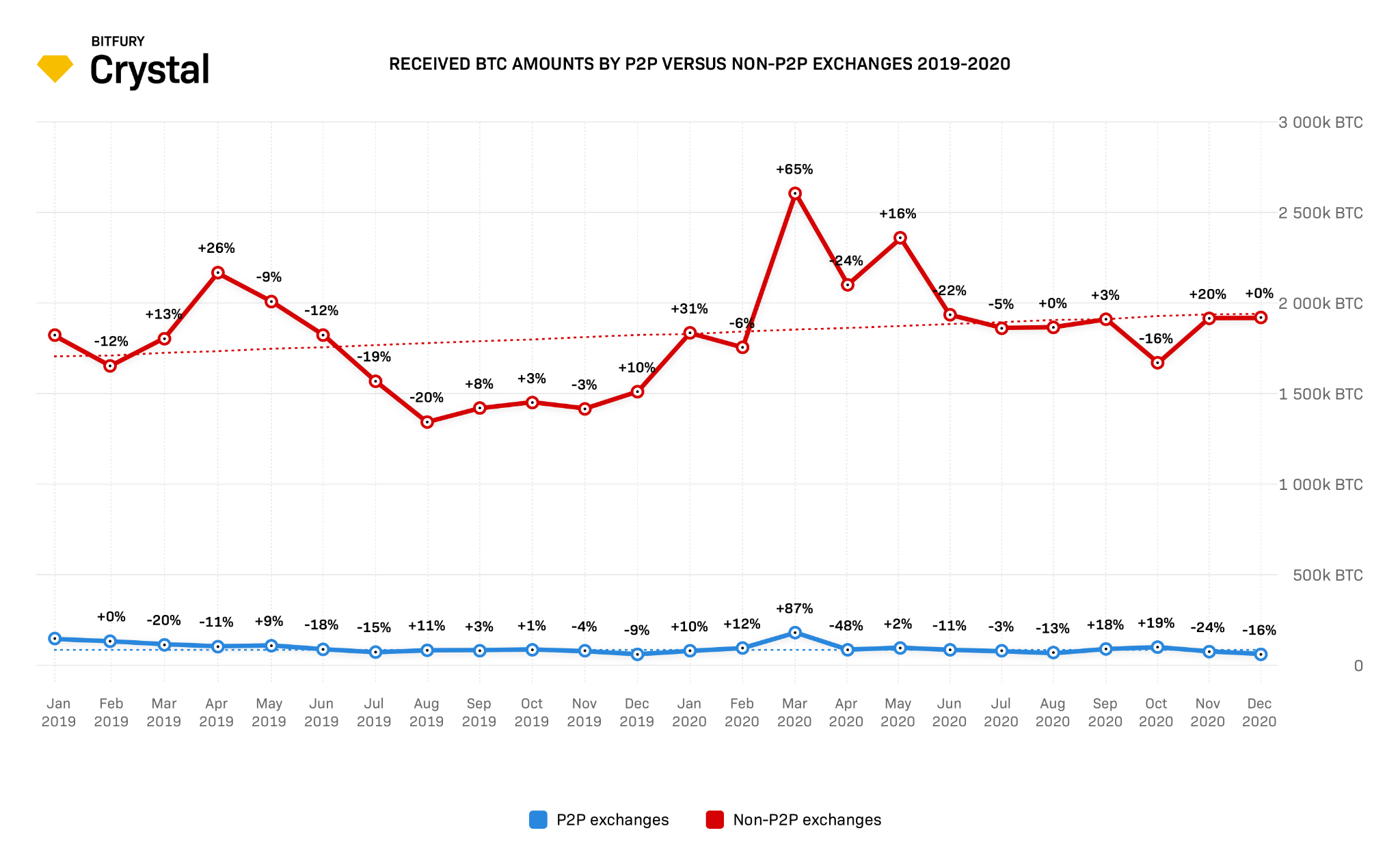

Despite CEX implementing KYC as a standard in order to enact at least in some domains a failsafe for money laundering, it only slovenly manages to do so taking under purview the importance of avoiding rigorous restrictions more so than the actual “secureness” of the platform. In the contemporary digital currency market and its rendition, a very implicative concern can be made about the uncertainty and general untrustworthiness of the digital currency equivalents. In the US alone there is a stark and relentless rise in malfeasant activities borne out from the crypto space. Specifically, new project launches have become a hotbed for gullible retail investors who are seeking a lucrative investment opportunity and ultimately fall prey to the derisively bold promises of enrichment of one's bank account. This can be attributed to the relative ease with which a potential investor can interact with the digital currency market circumventing centralized exchange and going straight to DEX, ill-equipped to the knowledge needed in order to be cognizant of incongruities with specifics of crypto investing. Relevantly, the outflow of retail investors from the centralized exchanges has also impelled a massive degree of popularity relay into decentralized alternatives of exchanges. In essence, DEX is poised beyond the reach of regulations and therefore is, on one hand, an unbridled way to trade and invest in digital assets but on the other hand is bristling with the unregulated in- and outflow of frequently fraudulent funds turnover. Unregulated and stripped of enforced compliance, DEX has garnered an unprecedented degree of recognition from market participants. This is attributed to the warranted fear about the unrestrained control and potentially oppressive influence of the governmental bodies, manipulating the to and fro movement of funds, completely omitting the individual jurisdiction over personal financial means. In this vein, DEX “entrusts'' a complete power over the financial means of every individual to the very same individuals without constricting the medium of financing and investing with custodian measures. There is no clear statistical data on DEX being a “Haven” for money laundering as it is often stigmatized by the media, there is however a great chart on the volumes of BTC transactions on so-called P2P exchanges or DEX.

Source: Crystalblockchain.com

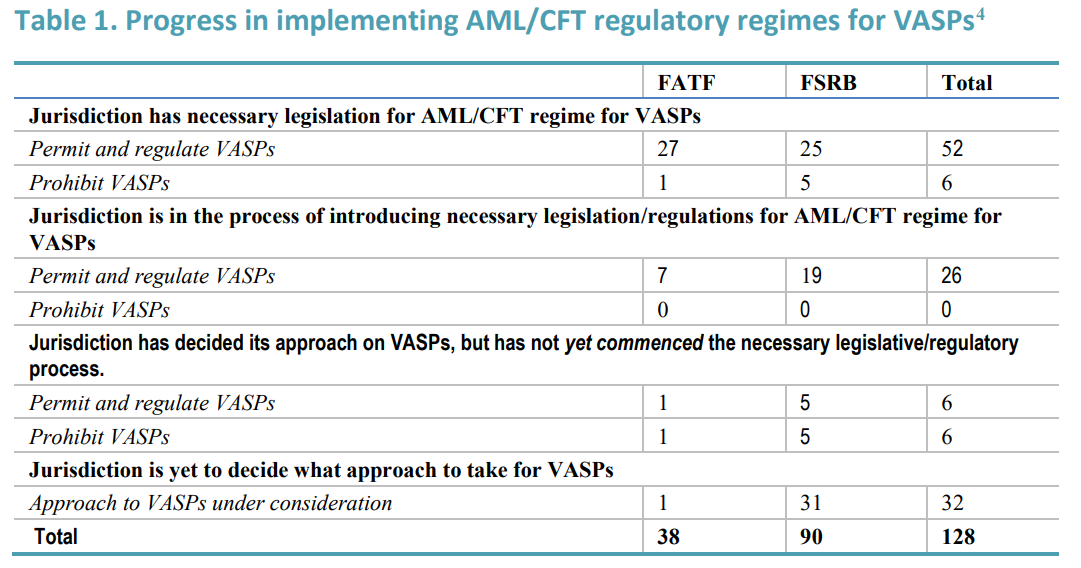

Crystal makes a correlative derivation from the data claiming that with the FATF stating that they will take rein over the P2P exchanges in June 2021, there is a steep decline in received amounts of BTC overall compared to centralized exchanges, denoting a potential disinclination from money laundering. The recent Plenary of FATF long-term review of the implementation of FATF’s revised Standards on virtual assets, noting that there is clear progress to a more collaborative effort toward rectifying the immediate issue with potential ML and FT incursion. \[...] “58 out of 128 reporting jurisdictions advised that they have now implemented the revised FATF Standards, with 52 of these regulating VASPs and six of these prohibiting the operation of VASPs. The private sector has made progress in developing technological solutions to enable the implementation of the ‘travel rule’.” Despite the progress being made, there is a predominantly listless reaction toward implementation of radical changes especially with the proposed “travel rule” that postulates a dangerous notion of “...all digital fund transfers creators and beneficiaries should exchange descriptive information” that unapologetically undermines the entire concept of decentralized exchange system and unavoidably creating an overt rebuttal from the DeFi community circles.

This unresolved issue creates a cleft between two groups namely market participants and regulators hindering mass adoption of digital ungoverned financing. While the goal of erecting compliant-ready solutions is valiant, the means proposed don’t align either with the community or the vision of the majority of projects themselves. Implementation of supervisory elements, centralized funds tracing heuristics, are derelicts of obsolete governmental overseers trying to impose strict and unnecessary bounds on the financial liberty of individuals. Despite FATF’s persistence on the introduction of custodian compliant protocols by propounding that potential future investors might be: “ \[...} disincentivize further investment in the necessary technology solutions and compliance infrastructure”, there is neither proof nor contingency to this statement. Certainly, it is crucial to minimize the frequency of fraudulent, illegal, and suspicious intrusions in the crypto space. However, it necessitates finding an appropriate compromise that is reached inferentially instead of carelessly exposing the whole structural integrity of blockchain to the unneeded and redundant custody. It should, however, be noted that despite the constant demonization of any type of regulatory measures in the crypto community, the majority of regulators and NGOs are in fact against outright discarding P2P exchanges and instead innovate in a way that would ultimately be beneficial in the wide scope and prolific adoption phase.\

\

Instead of FATF attempts to standardize the priority of AML for VASP (virtual asset providers), there is a patent unwillingness and pushback to do so. Blockchain data analysis groups such as Ciphertrace and Chainalysis do have their foot in the door in the provision of data, transactions retracement, and even deanonymization of peer-to-peer interrelations. However, the main contentious point about them is a centralized aspect of the operation and post-factum interception/analysis.

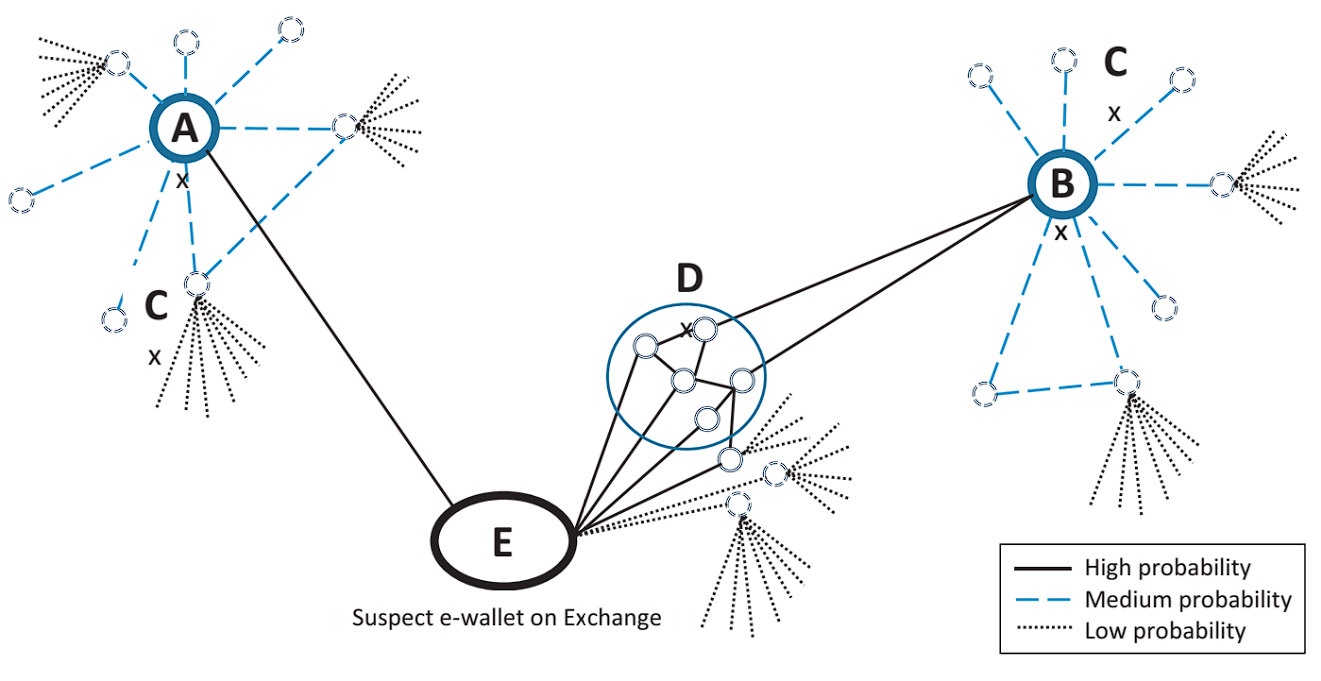

In AML compliant exchanges all traders are subjected to the disclosed environment that is easily traceable. Suspicious transactional activity can be easily impeded if the necessary suspicions are raised either from the governmental bodies or detected by automated systems. Each E-wallet on CEX that conducts fiat-to-crypto trading is marked and therefore CEX has a wide reach in terms of deriving data on the actions of users within it. For instance, if there is a node under suspicion of laundering money on the centralized exchange the system can automatically flag it accordingly and enact a proper verdict on the spot. Subordinated nodal wallets indicate a lower risk and exude less suspicion in general but still remain under the watchful eye of the system. Additionally, there is a possibility for CEX to also inhibit structuring or smurfing attempts i.e.prevent dissemination or regroup of funds inside the exchange to different wallets becoming the focal point of the investigative forces of the system.

CEX also widely utilizes the above-mentioned layers of AML security solutions that are mainly directed towards assessing the faultiness and inconsistencies of digital transactions. CypherTrace in particular is able to actively infer the likelihood of illegitimacy. This is done with the help of a plethora of advanced detection algorithms that use proprietary clustering techniques to link a wallet to transfers. Chainalysis on the other hand exclusively focuses on tracking Bitcoin transactional activity by tracking and collating in and output transactions inside the ledger establishing chronological and historical order of all of the transactions that a particular address has been engaged in.

##